5 Real Estate Business Goals Every SMART Investor Should Set

Goals are fuel. Goals are direction. Goals are what push us forward in life.

Here, are three (albeit lofty) definitions for the word “goal.” More formally, however, Wikipedia defines a goal as “the object of a person’s ambition or effort; an aim or desired result.” In other words, goals are just the tasks people assign themselves on a daily basis — that’s it.

The word goal tends to have a righteous aura about it. People who set goals are “over achievers,” or “those who set goals are superior to those who don’t.” Sometimes, goals are considered threatening or unattainable. But in all actuality, a goal can be as small as promising yourself you’ll do the dishes before you go to bed every night this week.

The problem with giving the word goal so much authority is that it turns the idea of goal settinginto something so intimidating nobody wants to give it a try. If we can all start to regard a goal for what it really is – nothing more than a daily chore – a greater number of people will prioritize setting goals and, thus, more people will accomplish their personal and professional ambitions. Remember, creating business goals is a great way to realize success on a higher level.

So, as an investor, which real estate business goals will best serve your bottom line and how will you go about achieving them in successful and efficient manner? Read on to discover the answer.

Real Estate Business Goals That Will Set You Up For Success

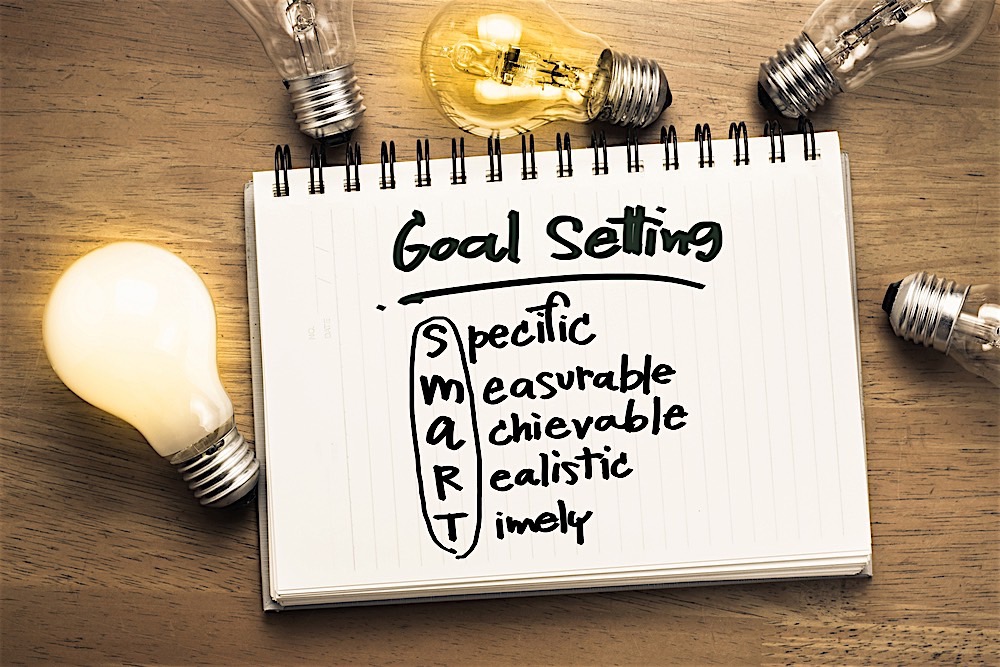

Did you know businesses that set clearly defined goals are 10 times more successful than businesses that don’t? A Harvard Business University study recently found that 83 percent of the population does not set goals and of those that do, 92 percent fail to achieve them. Number one: why are so few people setting goals? Number two: why aren’t more people succeeding in accomplishing those goals? The reason is simple: because the goals most people set aren’t setting smart.

- Specific

- Measurable

- Attainable

- Relevant

- Time-bound

S.M.A.R.T is an acronym you can use to guide your real estate business goal setting.

Fantasizing over your hopes and aspirations is far different from taking the time to sit down, put pen to paper, and set legitimate goals. Fantasies won’t produce results, while smart real estate business goals will take your business to new heights.

So let’s get into it, shall we?

Specific Real Estate Business Goals

Every real estate business goal you set should be as specific as possible. Clearly define every term within the goal and establish actionable steps to follow. If you want to improve this year’s revenue, your goal should be more than “I want to increase my profits.” Alternatively, “I want to increase this year’s profits so that I can increase next year’s marketing budget. I will start by evaluating my lead generation strategies and streamlining my systems. I will need the help of John Doe and Suzy Que to make this goal a reality.” While not necessary, it can be helpful to create a physical checklist for yourself and cross out each stage of the goal as you accomplish it. According to the same Harvard Business University study, writing down your goals makes you 14 percent more likely to achieve them; so why not go the extra mile to give yourself the advantage? When drafting your goal, be sure to ask yourself:

- What exactly am I trying to accomplish?

- Why is this goal important?

- How will achieving – or failing to achieve – this goal affect my business’ bottom line?

- What resources will I need to accomplish this goal?

- Who will need to be involved to successfully accomplish this goal?

If you have a valid answer for each of the above questions, your goal will meet the “S” criteria in the S.M.A.R.T acronym.

Measurable Real Estate Business Goals

Goals that are measurable will help you stay motivated by giving you the ability to track your progress. If you set goals that have metrics and KPI’s, you’ll be able to assess how much you’ve improved and how much work still needs to be done. When you take the time to track your progress, you’re more likely to meet deadlines and you will feel more excited as the finish line approaches. When your goals are not measurable, you’re more likely to get off track and distracted.

Let’s say you want to save up $20,000 by the end of the year. Instead of declaring such a broad statement, be more precise and say you will put an extra $1,000 into your savings account each week. This way, you can track exactly how much you’re conserving and can easily make up the difference if you accidentally skip one week.

Attainable Real Estate Business Goals

Often times, people set business goals that are so monumental, they become impossible to achieve. A brand new real estate investor shouldn’t expect to flip 40 properties in his or her first year on the job. If you truly want to be successful in accomplishing your goals, they must be realistic or else you’ll wind up feeling defeated; eventually, you will stop setting goals all together. The goals you set should still be challenging enough to push you to your limits and exhaust your resources, but practical enough to accomplish. Ask yourself:

- Am I financially ready to take on this goal?

- Have I given myself the necessary time to accomplish this goal?

- What constraints or hurdles do I expect to face when striving to accomplish this goal?

If you take the time to address every negative scenario that could keep you from achieving your goal and subsequently identify the solution you will use to solve that potential problem – supposing that it arises – you’ll be ready to take on whatever obstacle stands in your way.

Relevant Real Estate Business Goals

Setting goals that are relevant is all about ensuring that said goals matter to the current state of your business efforts. Establishing that you want to be CEO of a commercial real estate firm someday while you’re still wholesaling properties in your local market part-time to pay the bills would not qualify as “relevant”. Creating long-term goals is important; and dreaming of a more successful future is a great way to stay motivated. But in terms of helping your business’ bottom line, relevancy plays a more crucial role.

Time-Bound Real Estate Business Goals

This last step is pretty straight forward: give your goals a deadline. It is one thing say you want to improve your real estate education this year, it is another to say you will attend either a networking event, REI club meeting, or industry conference two times per month for six months. When you create a target date for achieving each individual goal, you are more likely to remain distraction-free. What will you do today, next week, six weeks from now and 3 months from now in order to accomplish your six month goal? How will your six month goal help you achieve your one year goals? How will you one year goals help you achieve your 5 year goals, and so on? In order to be successful, be sure to celebrate wins and milestones along the way to keep your energy tank on full.

Setting “smart” real estate business goals is the best way to achieve long-term success. So next time you catch yourself daydreaming of a financially free future, stop, and, instead, grab a pen and paper to ensure each goal you set is specific, measurable, attainable, relevant and time-bound.

see more at https://www.fortunebuilders.com/5-real-estate-business-goals